- About us

-

News & articles

Back

News & articles

View our latest company news and thought leaderships here.

See all the news stories - Products

- Underwriting teams

View our latest company news and thought leaderships here.

See all the news storiesTo view a pdf version, click here.

Although forward looking indicators have generally improved recently, the UK economy fell into recession in Q4 2023 when real GDP contracted by 0.3% quarter on quarter. While conditions are set to improve this year and the outlook generally brighter, growth is unlikely to exceed 1%.

Consumer Confidence

Consumer confidence is declining with British households struggling to manage a severe cost of living crisis in the immediate aftermath of the Covid pandemic. As a consequence, consumer confidence reached a new all-time low in 2022 with GfK’s Consumer Confidence Index dropping to -49 points in September. However, since then, the index has gradually recovered, coming at -19 points in early 2024.

On a positive note, all of the index’s five sub-ratings improved in January 2024 with consumers neutral about the prospects of their personal financial situation over the next 12 months. When it comes to major purchases, confidence is still in negative territory (-20 points, up from -40 one year earlier), but as the inflation picture brightens and with persistent, robust wage growth, we should see further improvements throughout 2024. As a result, companies operating in the B2C space can expect higher sales this year but several downside risks (see Real GDP Growth chapter) continue to cloud the outlook.

Business Confidence

Recent Purchasing Managers’ Index (PMI) data for the UK shows that conditions in the corporate sector continue to improve but surveys indicate that the manufacturing sector is lagging behind the construction and service sectors.

The UK manufacturing sector PMI came in at 47.5 points in March and while this is the best reading in ten months and an increase on February’s 47.0 points, it is still below the neutral 50-points line that separates expansion from contraction. For 19 consecutive months, manufacturing PMI has remained in contraction territory, highlighting the headwinds the sector is facing in the UK and Europe.

Encouragingly (and despite the problems in the Red Sea and Suez Canal), the supplier lead time sub-index improved in March, but this was more than offset by the four other index categories. Most worryingly, “new order inflow” remained in contraction territory, indicating that output will remain subdued in the months ahead. In fact, UK manufacturing production has now fallen for twelve consecutive months while new order inflow has been on a deteriorating trend for eleven months. New export business has contracted for 25 straight months now, mirroring international price competitiveness problems as well as post-Brexit pain.

Meanwhile, in the construction sector, the PMI stood at 48.8 points in February , an increase on the 46.8 recorded in the previous month and the best reading since August 2023. Although still below the neutral 50 points line, the latest survey leaves room to be cautiously optimistic about the year ahead.

Over half (51%) of the survey panel predict a rise in business activity in the next twelve months while only 12% forecast a contraction, the best level of business optimism in more than two years.

In the service sector (which accounts for 83% of UK employment and 81% of gross value added), the corresponding reading remained in growth territory for the third consecutive month. Reaching 54.3 points in January, the PMI now stands at the highest reading since May 2023 and new order inflow also stood above the 50-points line for the third time in a row. While demand from the Eurozone fell, this was offset by improving order volumes from Asia and the US.

More positivity comes from the strongest period of job creation in the sector since mid-2023 but survey respondents suggest that elevated wage pressures are acting as a drag on further increases (see Labour Market chapter). Output prices in the sector continue to rise, albeit by the slowest pace since September, and purchasing managers in the service sector are optimistic about 2024. Again, more than half (52%) of survey respondents expect business conditions to improve in the twelve months ahead, with only 12% feeling downbeat about their prospects.

The Composite PMI (which is the weighted average of manufacturing and service sector PMIs) also remains in expansion territory for the third consecutive month, reaching 52.9 points in January, the best reading since May 2023. With interest rate cuts on the horizon and inflation forecasted to fall throughout 2024, business optimism is set to improve further over the coming months and quarters.

Real GDP Forecasts

The British economy dropped into a lower gear during 2023. After quarter on quarter expansion of 0.2% in Q1, real GDP growth stagnated April to June before contracting in the second half of the year. Following a 0.1% drop in Q3, the economy fell into a technical recession in the final quarter of 2023 as real GDP decreased by another 0.3%. For the year as a whole, growth more or less flatlined (+0.1% against 2022), the worst annual performance (ignoring the Covid-distorted 2020-figure) since the global financial crisis in 2009.

Even more worryingly, real GDP per head fell by 0.7% in 2023 (as the British population continues to grow) and productivity growth is negative as well – Q4 saw a 1.% drop on the previous quarter and a 0.3% in year on year terms. Retail sales as well as manufacturing output both decreased in real terms in early 2024 and although the outlook for both sectors is gradually improving, 2024 will be another challenging year.

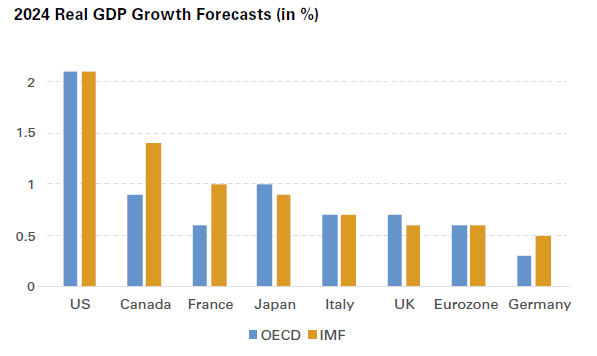

Real GDP growth projections for 2024 vary to a certain degree but the spread is small - KPMG expects the UK economy to expand by 0.5% this year , while EY has pencilled in 0.9% . The forecasts from the IMF (0.6%) and the OECD (0.7%) lie in the middle , cementing expectations of below 1%-growth in 2024. While this is poor on a historic comparison, it is very close to the anticipated rate of expansion in other European markets. Positively, companies operating in the UK can expect slightly improving macroeconomic conditions but the magnitude of the anticipated upturn will be limited.

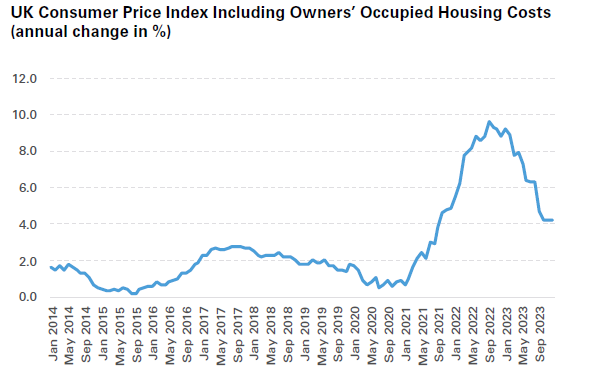

Encouragingly, inflation remains one of the bright spots of the British economy. After having risen to a 41-year high of 11.1% in late 2022, price pressures have subsequently moderated and inflation has dropped back to 4.2% in January 2024 . Although this is still more than twice above the Bank of England’s (BoE) 2% target, the development is welcome news for households which had seen their disposable incomes squeezed. In line with developments in the Eurozone, inflation rates in the service sector are currently exceeding manufacturing inflation.

According to the Office for National Statistics (ONS), goods inflation stood at 1.8% in January but services inflation still came in at 6.5%. More positively for consumers, food price inflation continues to ease at a rapid pace, coming down from 8.0% in December 2023 to 6.9% in January 2024, the lowest annual rate since April 2022 . The recent drop was the tenth consecutive monthly improvement and food price inflation is now down considerably down from the 45-year high of 19.2% in March 2023.

Looking ahead, inflation is likely to continue to fall for a number of reasons - base effects, the consequences of aggressive monetary tightening in 2022-23, lower commodity prices and poor economic growth figures. The Office for Budget Responsibility (OBR, a public body funded by the UK Treasury to provide independent economic forecasts and analysis) recently published a new set of projections alongside the Spring Budget on 6 March.

According to this analysis, inflation will drop below the 2% target in Q2 2024, around a year earlier than expected . For the year as a whole, the OBR expects consumer price inflation to come in at 2.2% before falling to 1.5% in 2025. However, given the uncertainty around geopolitical events, energy prices and other factors impacting inflation, the OBR stresses there is a 10% chance of consumer prices rising by more than 4% in 2025 or dropping below -1% that year.

Unemployment

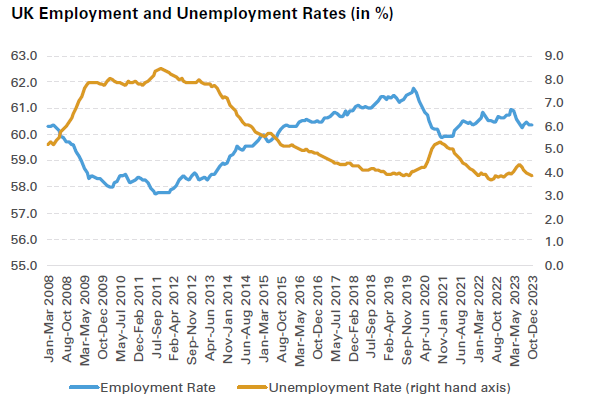

Despite the economy falling into recession in late-2024, the UK labour market is holding up well. The unemployment rate came in at 3.8% in Oct-Dec 2023, down from 4.3% in mid-2023 and close to the full-employment definition used by many economists . Furthermore, the employment rate continues to hover around the 60% mark, down from 61.8% before the outbreak of the Covid pandemic but virtually unchanged since mid-2020.

Source: ONS

According to the latest OBR forecasts from early March 2024, unemployment will increase somewhat over the coming months, reaching 4.5% (equivalent to 1.6m workers) by the end of the year, before gradually subsiding again. For 2025, the OBR predicts an unemployment rate of close to 4% .

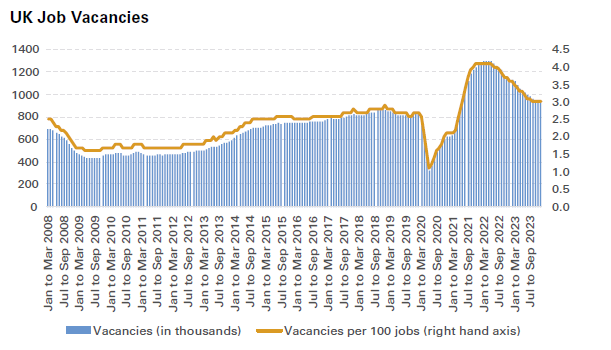

Vacancies

While the unemployment rate has yet to respond to the slowing economy (it is unlikely to do so in any significant way in 2024-25), the number of job vacancies draws a slightly different picture and indicates a cooling down of the labour market. Coming in at 932,000 in November 2023 to January 2024, vacancies have fallen on the quarter for the 19th time in a row. In an annual comparison, figures are down by around 18% and 17 out of the 18 sectors surveyed reported a smaller number of open positions. Although overall levels still exceed pre-pandemic readings (in early 2020, the number of vacancies was around 130,000 lower) there are four industries where the number of unfilled positions now stands below pre-Covid readings, with the largest drop reported in wholesale and retail trade.

While recruiting still remains a challenge, recent survey data shows that job retention has become a less pressing concern in recent months . Nonetheless, companies will continue to struggle to find new workers. This is particularly problematic in the accommodation and food services sector (4.5 open positions per 100 jobs) and the human health and social work sector (3.9 per 100), compared with the national average of 3.0.

Wage Growth

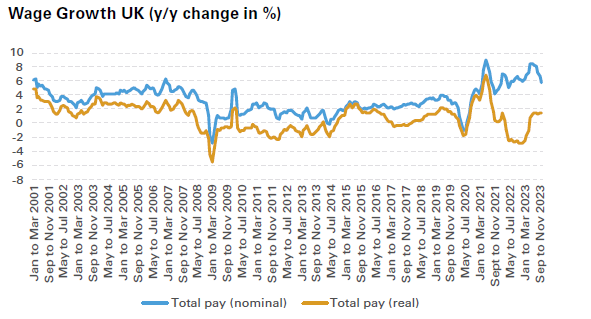

Similarly, salary developments in the UK economy also point towards a modest cooldown in the labour market. Nominal wage growth has continued to ease from the levels recorded in 2023 when salaries increased by 7% year on year, the highest rate of growth rate in 30 years (omitting distorted figures from the Covid period). This was driven by a tight labour market as well as very high inflation (see Inflation chapter) which resulted in high wage settlements . In real terms (adjusted for inflation), the increases were much more modest with ONS data showing that in October-December 2023, real wages increased by 1.4%, more or less unchanged since mid-2023.

Data: ONS

According to the OBR, 2024-nominal wage growth will be somewhat stronger than anticipated as, despite falling inflation, wage settlements continue to be strong. For this year, the OBR forecasts salaries will increase by 5%-5.5% which would translate into real wage growth of above 3% (as inflation is coming down) . While this boosts disposable income for households and helps to shore up domestic demand, it also leads to a higher cost base for companies which in turn leads to higher credit risk levels. Positively for companies’ wage bills, nominal wage growth should stabilise to around 2% in 2025-26, falling in line with stagnant real wages.

As the economy dropped into lower gear in 2023 and a technical recession, credit risk in the UK has also risen. While B2B payments performance has not yet responded to the poor real GDP growth rates and the sharp monetary tightening, insolvency risk increased last year and is likely to remain on this worrying trend.

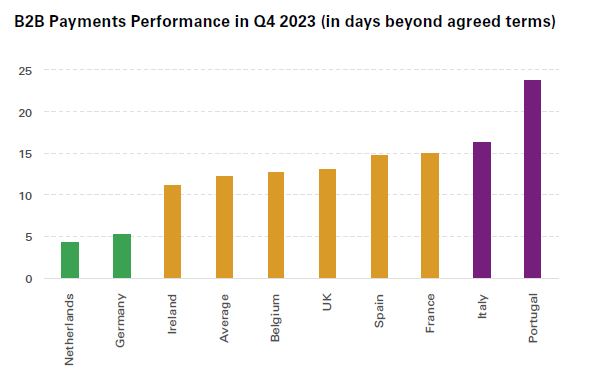

On a more positive note, data from business information provider Dun & Bradstreet and its European partners shows that B2B payments performance in the region has not deteriorated yet, despite the strong economic headwinds. In early 2023, average payment delays (measured in days beyond agreed terms) in Europe stood at 12.4 days, improving slightly to 12.1 days by Q4 2023 . In the UK, the improvement was even more marked: in Q1, delays stood at 13.9 days but by Q4 2023 this figure had dropped to 13.1 days.

In a regional comparison, the UK continues to rank mid-table. The Netherlands and Germany remain at the top of the league with delays of 4.2 days and 5.2 days respectively, while Ireland has recorded a sizable improvement in October-December 2024 (from 12.0 days in the previous quarter to 11.1 days). Positively, the UK continues to outperform the Southern European states. While Spain, Italy and Portugal have traditionally scored poorly, France’s ranking has slipped over recent quarters with payment delays across the Channel rising from 12.9 days in early 2023 to 14.9 days today.

The developments in the UK (and in other European markets) are somewhat surprising as the slowing economy and the high interest rate environment should have resulted in poorer payments performance. That said, the indicator tends to lag the economic cycle by a few quarters so those slower payments could emerge as 2024 develops.

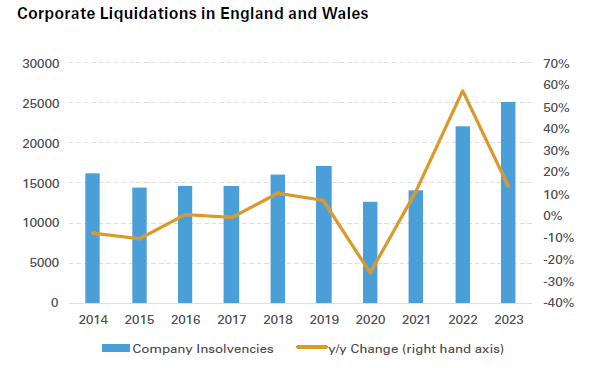

Unlike payments performance, the business failure rate deteriorated sharply in 2023. In England and Wales, the Government’s Insolvency Service recorded 25,158 company insolvencies in 2023, the third consecutive annual increase (up by 13.7% against 2022) and the highest reading since 1993. The number of creditors’ voluntary liquidations was the highest since the data series started in 1960.

Worryingly, liquidation rates also soared last year. One in 186 active companies entered insolvency liquidation in 2023, translating into a rate of 53.7 per 10,000 active businesses. This is an increase on the 49.6 recorded in 2022 and the 2023-reading was the poorest since Q3 2014. Despite the overall number of insolvencies skyrocketing to a 30-year high, the liquidation rate is nowhere near the readings seen during the global financial crisis in 2008-09 when it reached 94.8 per 10,000 active companies. This is because of more businesses being registered with Companies House nowadays.

Looking ahead, the number of business failures in the UK is likely to increase further for a number of reasons. Firstly, the weak real GDP growth recorded in 2023 (which is set to last into this year) will have a delayed negative effect on business failures. Secondly, interest rates have increased substantially in 2022-23 and although cuts in the second half of 2024 are likely, given the lower inflation rate and the weak economic performance, the effects of this monetary loosening will not be felt immediately. Thirdly, banks tightened lending terms in 2023, a development likely to continue.

These issues are limiting the ability of companies to take out new loans or roll over existing debt. Against this backdrop, counterparty risk should be monitored closely and appropriate action (such as tightening credit terms or leveraging trade credit insurance) should be considered.

By Ray Massey, Underwriting Director, Credit

Disclaimer

The information contained in these articles and documents are believed to be accurate at the time of date of issue, but no representation or warranty is given (express or implied) as to their accuracy, completeness or correctness. TMHCC accepts no liability whatsoever for any direct, indirect or consequential loss or damage arising in any way from any use of or reliance placed on this material for any purpose. The contents of these articles/documents are the copyright of Tokio Marine HCC. Nothing in these articles/documents constitutes advice, nor creates a contractual relationship.

Related links

https://www.gfk.com/press/consumer-confidence-up-three-points-to-19-in-january

https://www.pmi.spglobal.com/Public/Home/PressRelease/2e8a940722ea4e8ca424ae620e78263f

https://www.pmi.spglobal.com/Public/Home/PressRelease/a1c11bfd622940cc9681c3423e2fba35

https://www.pmi.spglobal.com/Public/Home/PressRelease/983758bd175848c78f10343dc3ec8e84

https://www.ons.gov.uk/economy/grossdomesticproductgdp/bulletins/gdpfirstquarterlyestimateuk/octobertodecember2023

https://researchbriefings.files.parliament.uk/documents/CBP-9040/CBP-9040.pdf

https://kpmg.com/uk/en/home/insights/2018/09/uk-economic-outlook.html

https://www.ey.com/en_uk/news/2024/01/uk-economy-stagnation-should-start-to-fade-in-2024

https://commonslibrary.parliament.uk/research-briefings/sn02784/

https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/consumerpriceinflation/january2024

https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/consumerpriceinflation/january2024

https://obr.uk/docs/dlm_uploads/E03057758_OBR_EFO-March-2024_Web-AccessibleFinal.pdf

https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/employmentandemployeetypes/bulletins/employmentintheuk/february2024

https://obr.uk/docs/dlm_uploads/E03057758_OBR_EFO-March-2024_Web-AccessibleFinal.pdf

https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/employmentandemployeetypes/bulletins/jobsandvacanciesintheuk/february2024#vacancies-for-november-2023-to-january-2024

https://obr.uk/docs/dlm_uploads/E03057758_OBR_EFO-March-2024_Web-AccessibleFinal.pdf

https://obr.uk/docs/dlm_uploads/E03057758_OBR_EFO-March-2024_Web-AccessibleFinal.pdf

https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/employmentandemployeetypes/bulletins/averageweeklyearningsingreatbritain/february2024

https://obr.uk/docs/dlm_uploads/E03057758_OBR_EFO-March-2024_Web-AccessibleFinal.pdf

https://cdn.informa.es/sites/5c1a2fd74c7cb3612da076ea/content_entry5c5021510fa1c000c25b51f0/65e1b11f77974600ca1b0b49/files/Pagos_europaT42023_es.pdf?1709289759

https://www.gov.uk/government/statistics/company-insolvency-statistics-october-to-december-2023/commentary-company-insolvency-statistics-october-to-december-2023#company-insolvency-in-scotland