- About us

-

News & articles

Back

News & articles

View our latest company news and thought leaderships here.

See all the news stories - Products

- Underwriting teams

View our latest company news and thought leaderships here.

See all the news storiesTo view a pdf version, click here.

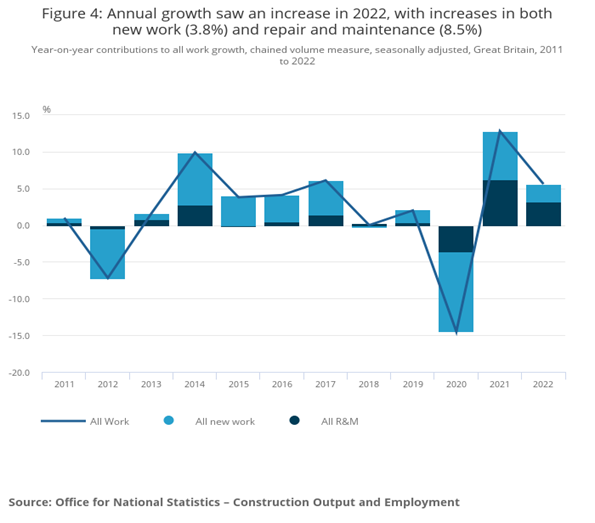

Following a stellar 2021, when construction sector output in the UK increased by a record 12.8%, industry performance normalised somewhat last year. Data from the Office for National Statistics (ONS) shows that total annual construction sector output expanded by 5.6% in 2022 with both new work (+3.8%) and repair & maintenance (+8.5%) making positive contributions to growth. Out of the industry’s nine sub-sectors, four shrank with “public other new work” recording its sixth consecutive contraction while “private commercial” saw a drop for the fifth straight year.

Chart: Annual Output Growth

Worryingly however, ONS data also indicates that the sector is running out of steam with growth in the second half of the year slowing down markedly: output growth dropped from 3.0% quarter on quarter (q/q) in January-March to 1.5% in April-June before declining further to 0.3% in each, Q3 and Q4 2022.

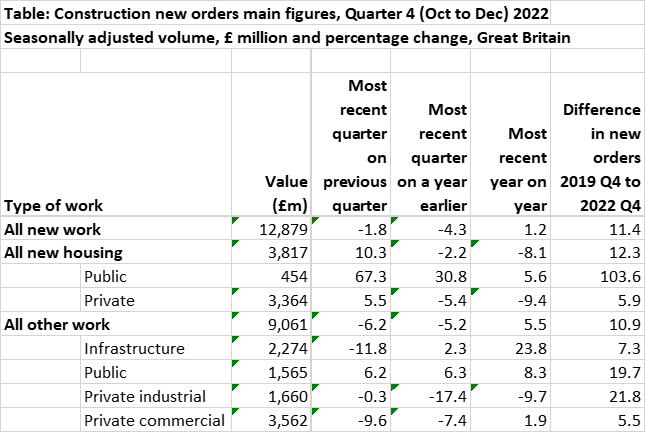

Also problematically, new order inflow has seen a dip in late 2022, indicating further troubles ahead. For the year as a whole, the UK construction sector recorded a 1.2% increase in new orders but when compared with Q3, the final quarter of the year saw a 1.8% drop. This was mainly caused by the “infrastructure” (down by 11.8% q/q) and “private commercial” (-9.6%) sub-groupings while “private new housing” still recorded a 5.5% increase in October-December 2022.

Table: Construction Sector New Orders

Source: ONS and Barbour ABI

Sector confidence mirrors the ONS new order inflow data with the S&P Global and CIPS UK Construction

Purchasing Managers’ Index (PMI) for January showing another drop in the headline figure from 48.8 in December

to 48.4 points. The 50-point mark divides expansion in sectoral activity from contraction and this poor

reading was mainly driven by the house building sub-index (44.8 points - a 32-month low) while commercial activity

(48.2 points) and engineering activity (49.7 points) held up better.

The employment PMI measurement also deteriorated for the second straight month and purchasing activity dropped to the lowest reading since lockdown in May 2020. Against this backdrop and the expected 2023 headwinds, it is somewhat surprising that the business expectations sub-index has rebounded strongly from its 31-month low in December and is now on the highest reading since mid-2022. Nearly half (43%) of survey respondents expect an increase in business activity in the twelve months ahead, compared with 17% who forecast a deterioration.

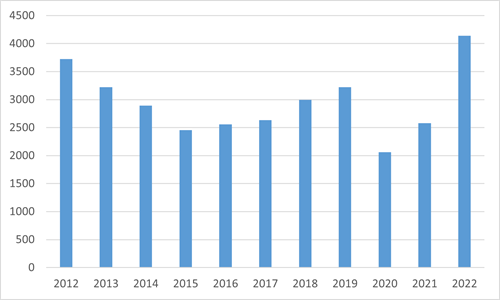

In terms of bankruptcies, the sector continues to account for a high share of UK business failures. Although only representing 7% of the British economy, the construction sector accounted for 18.7% of all bankruptcies in England and Wales in 2022, according to the Government’s Insolvency Service. Worryingly (but in line the overall trend), the number of business failures increased greatly in 2022. While the overall figure in England and Wales grew by 57.3% last year (to 22,109 registered company insolvencies), the construction sector saw a 60.5% increase (to 4,143 bankruptcies). In a historic comparison, the 2022 figure is almost as high as the (artificially Covid-supressed) 2020 and 2021 readings combined and the highest since the global financial crisis in 2008-09.

Chart: Registered Company Insolvencies in the Construction Sector in England and Wales

Source: Insolvency Service

Over the last few decades, the UK construction sector has gone through a process of fragmentation with many companies classed as small or even micro companies. These firms traditionally hold little or even no reserves which raises questions about the sector’s ability to withstand negative shocks. The number of workers employed in the sector increased from 1.29 million in 2007 to 1.39 million in 2021 (up by 8.2%). During the same period, the number of firms grew from 192,000 to 353,000, equivalent to an 83.9% increase. The latest available ONS data for 2021 also shows that more than 81% of all construction companies in the UK have fewer than four employees while only 1,221 companies (out of a total of 353,365) had 80 or more workers. In terms of annual turnover, 82% of all construction companies in the UK generated less than £500,000 while only 9.4% had a turnover of more than £1m per annum. In this light, a deterioration of market conditions is likely to accelerate weaker payments performance and even higher business failures.

Unfortunately, a combination of interlinked factors make for a rather bleak outlook for the sector this year. In

terms of macroeconomics, the UK might narrowly avoid falling into recession in 2023 as forward-looking indicators

have improved somewhat in recent weeks. That said, the IMF forecasts that British real GDP will shrink by 0.6% this

year, adding further pressure to the construction sector.

From a monetary policy point of view, the sharp tightening cycle in recent quarters is bad news for the sector. As

inflation spiralled out of control on 2021-22, the Bank of England’s (BoE) key policy rate increased from 0.1%

in November 2021 to 4.0% in February 2023. Inflationary pressures have eased somewhat in late 2022 and early 2023

but with 10.1% in January, consumer price inflation still stands five times above the BoE’s 2% target which

means further interest rate hikes are likely. Markets are expecting a terminal rate of 4.5% with rates unlikely to

be cut before next year. This is unwelcome news for the building industry as it will be another drag on the

affordability of housing and property investment.

In this light, tighter lending conditions, as indicated in the BoE’s latest Bank Lending Survey, will also

adversely impact debt affordability in the UK and reduce demand in the construction sector. Latest data from the ONS

shows that prices for new construction work have been rising by double digits year on year since May 2022 and while

house prices have started to come down in a month on month comparison in December, they were still up by 9.8%,

compared with last year.

In addition to the negative macroeconomic backdrop and high interest rates, a tight labour market will weigh on

companies’ ability to expand operations in 2023. Although slightly down from its peak in early 2022 (as the

economy has cooled down in recent quarters), there are still more than 1.1 million job vacancies in the UK. This is

roughly 300,000 above pre-Covid readings. In the construction sector, 43,000 jobs cannot be filled at the moment and

for every 100 employees, there are 2.9 vacancies (slightly below the national average of 3.7 vacancies per 100

employees with accommodation and food services being hit the hardest with 6.6 vacancies per 100 workers).

On the supply side, the sector will continue to suffer from record high prices for land which will limit building

activity. In this context, the Government’s decision to drop mandatory house building targets in late 2022

will also have a negative effect. In the five weeks following the national Government’s announcement to

abandon this 2019-election campaign promise, nine local authorities have already paused or scaled back their plans

and further councils are likely to follow suit.

Furthermore, the Government’s plan to create a carbon-emission free economy by 2050 will also continue to

impact on the UK construction sector as currently, 30% of the country’s CO2 emissions originate from the built

environment (which also includes infrastructure). Of all British emissions, 7% are created during the manufacturing

and construction stage (“embodied emissions”) while 19% are generated in the operation of buildings,

mainly via heating (“operational emissions”). Worryingly, according to a report published by the Royal

Academy of Engineering, the sector is not on track to meet the ambitious targets given by the Government: by 2030,

carbon emissions created by UK construction companies should drop by 68% (compared to 1990 levels). On a practical

level the technology to remove the carbon intensive equipment is still woefully underfunded and without much needed

investment it will be very difficult to hit the target.Table: Growth in the value of underlying project-starts

(under GBP100m) by sector.

|

y/y change (in %) |

2021 |

2022e |

2023f |

2024f |

|

Private Housing |

30 |

-4 |

-5 |

15 |

|

Social Housing |

16 |

-9 |

-3 |

0 |

|

Industrial |

59 |

25 |

-5 |

-8 |

|

Offices |

27 |

4 |

5 |

-3 |

|

Retail |

39 |

-11 |

-4 |

10 |

|

Hotel & Leisure |

37 |

-6 |

9 |

2 |

|

Education |

14 |

-15 |

13 |

5 |

|

Health |

3 |

2 |

-6 |

1 |

|

Community & Amenity |

3 |

36 |

0 |

2 |

|

Civil Engineering |

12 |

-4 |

1 |

3 |

|

Total |

25 |

-2 |

-2 |

6 |

Source: Glenigan, Construction Industry Forecast 2023-24

Taking all factors into account, 2023 is set to be a challenging year for the British construction sector. According to Glenigan’s Construction Industry Forecast for 2023-24, private housing will start to drop by 5% this year with social housing also projected to see a 3% drop. While office starts are expected to grow by 5%, industrial construction will contract by 5% and retail will record a 4% drop. Civil engineering will flatline (up by a mere 1%) but building starts in the education sector are forecast to expand by an encouraging 13%, although there was a 13% contraction in 2022. All in all, total growth in the value of underlying project starts in 2023 is projected to shrink by 2% (on top of the 2% reduction seen in 2022) before the sector will start to recover somewhat in 2024.

Click here to visit our Whole Turnover Credit page for more information

Related links

https://www.pmi.spglobal.com/Public/Home/PressRelease/f1b9d60ec7f44ed49dcca1bf5cb74945

https://news.sky.com/story/building-firms-going-bust-at-fastest-rate-since-financial-crisis-12770697

https://www.gov.uk/government/statistics/company-insolvency-statistics-october-to-december-2022

https://news.sky.com/story/building-firms-going-bust-at-fastest-rate-since-financial-crisis-12770697

https://www.gov.uk/government/news/uk-house-price-index-for-december-2022

https://www.theguardian.com/society/2023/jan/15/new-homes-at-risk-as-english-local-authorities-cut-housebuilding-plans

https://www.lexology.com/library/detail.aspx?g=70973dcc-6604-411d-8d37-192dd714dcf2

https://raeng.org.uk/news/construction-sector-must-move-further-and-faster-to-curb-carbon-emissions-say-engineers

https://www.glenigan.com/market_analysis/construction-industry-forecast/